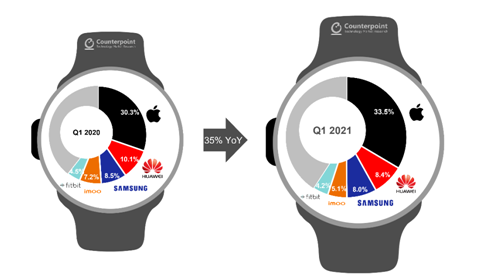

According to Counterpoint Research, the global smartwatch shipments in Q1 2021 has increased 35% YoYo. According to the report Apple has maintained its leadership position, by catalysing the overall market growth by recording a 50% YoY increase in the demand for the new Series 6 models. Apple consolidates as a leader in this segment by registering 50% annual growth which is capturing a third of the smartwatch market in terms of volumes.

Key Findings of Report

- Apple consolidates as a leader in this segment by registering 50% annual growth, capturing one third of the smartwatch market in terms of volumes

- Samsung to launch a mid-price-tier model to boost growth

- The merger of Wear OS, Tizen OS and Fitbit OS will further drive consolidation of the fragmented smartwatch market

- Wearable devices and services are going to become important

With the sale of Galaxy Watch 3 and Galaxy Watch Active series, Samsung’s shipments also rose 27% YoYo. These volumes include basic smartwatches with low-level proprietary OS or RTOS (like from Xiaomi and OPPO), kids smartwatches (like from BBK, Huawei and Vodafone Neo) and high-level smartwatches (like from Apple, Samsung, and Garmin).

Limat Counter Research added “Huawei continued to face headwinds because of the declining smartwatch sales and how well Huawei watches are optimized for its smartphones. Will be interesting to see when Huawei launches its first watch based on Harmony OS, as it hinted at the Huawei Analyst Summit last month. This should kickstart a new ecosystem for developers to build experiences for the wrist. But it will warrant a Harmony OS phone as well for the complete experience. HONOR, spun off from Huawei, should open up new opportunities for players such as Google and Qualcomm.”

Exhibit 1: Global Smartwatch Shipments Share, Q1 2021 vs. Q1 2020 (in %)

Senior Analyst Sujeong Lim feels that Apple has been able to further solidify its leadership position in the market by widening the portfolio from Watch SE to Series 6 at the right time. This might drive Samsung to launch a mid-price-tier model to boost growth.

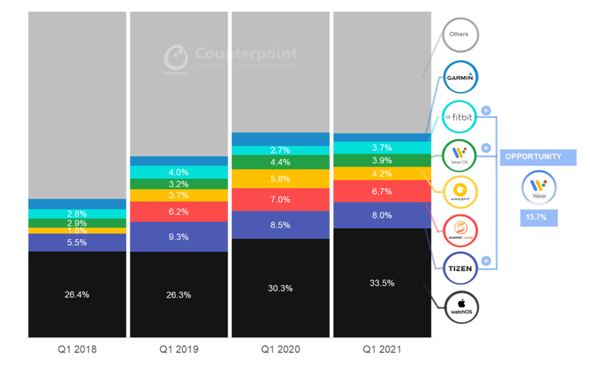

Apple’s WatchOS captured more than a third of the market with a growing attach rate to its base of billion iPhone users. It has been observed that in terms of smartwatch OS platforms,Google’s Wear OS has not yet achieved such success in smartwatches as most of the major smartwatch brands have developed and installed their own proprietary OS (like Fitbit OS, Tizen and Garmin OS). Further, Wear OS has been lacking behind in terms of features, battery optimization and chipset support. This has limited its share to a mere 4% of the global smartwatch market.Google is likely to integrate Tizen OS with Google Wear OS to reinvigorate the market and go full force after the 3.5 billion Android user base.

Lim said, “Hopefully, Google’s new Wear platform will be shipping in the next generation of the Galaxy Watch series in late Fall. It will be good for the companies involved. The focus would be to not only improve performance, such as battery life, but also improve on the AI, newer apps and services, and integration with Android smartphones. Samsung will also be able to better target the broader Android smartphone user base. With the completion of the acquisition of Fitbit, Google should be able to enhance the Wear platform with ‘fitness’ capabilities and services integration, moving forward.”

Exhibit 2: Global Smartwatch Shipments Share by Operating System (in %)

Vice President Research Neil Shah is of the view that the Google-Samsung announcement was a great move by Google to accelerate its ambitions for the wearables space. This initiative will build a robust portfolio of Wear devices integrating the best of all the three worlds – Tizen OS, Wear OS and Fitbit OS.

Highlighting why there is so much excitement for wrist wearables among tech companies, Shah said, “Wearable devices and services are going to become important for companies such as Apple, Google, Facebook and Amazon as they increasingly expand their reach in healthcare, pharmaceutical and insurance verticals directly or indirectly. This can include selling services such as Apple Fitness+, predictively cross-selling medicines and healthcare solutions, or attracting marketers to their ad platforms based on the health profiles built with the enormous amount of data generated via the number of sensors on these wearable devices. Further, addition of advanced voice AI and ML capabilities on these devices will make wrist as one of the key segments technology companies will go after this decade before adding eyes/brain-based advanced wearable devices to the mix.”