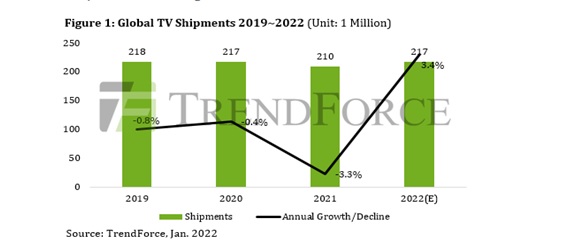

The shipment performance of TV brands in 1H21 benefited from COVID-19 economic relief funds in the U.S., driving a continuing boom in North American shipments. At the same time, TV brands continued to replenish panel inventories, pushing up panel prices. As the pandemic slowed down in Europe and the United States in 2H21, life returned to normal and pandemic stimulus no longer applied, challenging demand levels. In addition, rising raw material and freight prices pushed up whole device cost, forcing TV brands to pass costs onto retail pricing. Even though TV brands staked their hopes on the two major annual yearend sales promotion events of Singles Day in China (the biggest shopping day of the year globally, online and IRL) and Black Friday, sales performance was poor due to high costs leading to a slump in end-user demand and eventually causing TV shipments to decline by 3.2% annually to 210 million units in 2021.

It is indicated that panel supply and overall production capacity will be ample in 2022, dispelling severe TV panel price fluctuations while ushering in steady and moderate fluctuations as a replacement. After a sharp revision in TV panel prices in the 2H21, this year’s panel pricing is more advantageous to the planning of TV brands. In addition, the severe impact of the pandemic in Southeast Asia and emerging markets and high panel prices last year caused TV brands to reduce the scale of small-sized 23.6-inch, 32-inch, and 43-inch products, forcing a deferral of demand. In 2022, the pricing of small-sized panels will be close to panel manufacturers’ cash cost which will help TV brands recapture a larger proportion of small-sized panel shipments. The proportion of shipments below 39-inch will remain at 25%, medium-sized 40~59-inch panels will remain at 55%, and large-sized panels above 60-inch will remain the focus of international brands with market share expected to rise to 20%. Benefiting from the deferral of small-sized panel demand, TV shipments in 2022 will grow by 3.4% to 217 million units.

In 2021, OLED TVs benefited from soaring LCD prices in the previous two years. This was also the case with 55-inch 4K O/C products. The price difference between the two has narrowed from a multiple of 4.7 in early 2020 to 1.8 in mid-2021, thereby incentivizing more TV brands to switch to producing OLED TVs when LCD panel supply is limited and driving OLED TV shipments to 6.7 million units in 2021, or 70% growth YoY. Although Samsung Electronics intends to join the white OLED camp and simultaneously launch QD OLED TVs this year, the continuing falling pricing of LCD panels and the price of OLED TV panels (subject to LG Display’s strategy of increasing pricing as opposed to dropping them) may disrupt Samsung Electronics’ rollout of OLED TVs. If Samsung Electronics fails to launch spring OLED TV models, its original shipment target of 1.5 million units will inevitably be affected. However, whether it launches OLED TV models in spring or summer, Samsung Electronics will take advantage of its brand and channel advantages irrespective of other considerations to take the OLED TV market by storm and aim for a market share of 15%.

TCL has opened up new horizons for TV products after releasing its first Mini LED TV in 2020. In 2021, Samsung Electronics launched a series of 50-85-inch mid/high-end 4K and flagship 55-85-inch 8K Mini LED models, with shipments exceeding one million units in the first year, reaching 1.5 million units, and boosting overall Mini LED TV shipments in 2021 to 2.1 million units. In addition to Samsung Electronics and TCL continuing to utilize Mini LED in 2022, more TV brands will also join the fray. Overall Mini LED TV shipments will race towards 4.5 million units. SONY showed its 8K 85-inch and 75-inch TVs for the first time at CES at the beginning of the year. Sony’s flagship 4K 85-inch, 75-inch, and 65-inch models were the most notable at CES and Sony will join Samsung and LG Electronics as another international brand marketing OLED and Mini LED TVs, intensifying competition in the high-end TV market.

If you have an interesting Article / Report/case study to share, please get in touch with us at editors@roymediative.com/ roy@roymediative.com , 9811346846/9625243429.